بطاقة FAB Rewards Signature Credit Card الائتمانية

FAB Rewards Signature Credit Card Review 2026: Premium Rewards Without the Premium Fee

فريق المراجعة:

- 📝 الكاتب: أحمد حسن، CFP®

- ✓ مدقق الحقائق: سارة الخالدي، CFA Level II

- 🔍 المراجع: محمد عبدالله، خبير بطاقات ائتمان

- ✏️ المحررة: إنجي، رئيسة التحرير

آخر تحديث: مارس 2026 | المراجعة القادمة: يونيو 2026

⚠️ إفصاح مهم: قد نحصل على عمولة تابعة عند التقديم على بطاقة من خلال الروابط في هذه المراجعة، دون أي تكلفة إضافية عليك. هذا يساعدنا في الحفاظ على استقلالية المحتوى وتقديم مراجعات شاملة ودقيقة. سياسة الإفصاح الكاملة

📋 إخلاء المسؤولية: المعلومات المقدمة في هذه المراجعة هي لأغراض تعليمية ومعلوماتية فقط، وليست نصيحة مالية شخصية. يُرجى استشارة مستشار مالي مرخص قبل اتخاذ أي قرارات مالية. الشروط والأحكام قابلة للتغيير من قبل البنك المصدر.

Quick Verdict

The FAB Rewards Signature Credit Card delivers premium-tier benefits at a mid-tier price. With 2X points on dining, groceries, and petrol, complimentary airport lounge access (6 visits/year), and a reasonable AED 500 annual fee (free year one), this card offers exceptional value for professionals who want rewards flexibility. The ability to convert FAB Rewards points to Emirates Skywards miles, Etihad Guest miles, or cashback makes it one of the UAE’s most versatile rewards cards.

FAB Rewards Signature: The Versatile Rewards Champion

First Abu Dhabi Bank’s Rewards Signature Credit Card sits in the sweet spot between everyday cards and premium offerings. It’s designed for UAE professionals earning AED 15,000-25,000 monthly who want meaningful rewards and premium perks without paying AED 1,500-3,000 annually for cards like American Express Platinum or Emirates NBD Skywards Infinite.

The card’s strength is versatility. Unlike airline co-brand cards that lock you into one program, FAB Rewards Signature lets you convert points to Emirates miles, Etihad miles, or cold hard cashback. This flexibility ensures you’re never trapped in a loyalty program you don’t use.

Who Should Get This Card?

- Flexible Travelers: Those who fly multiple airlines and don’t want to commit to a single program

- Dining & Grocery Spenders: Households spending AED 3,000+ monthly on food

- Occasional Flyers: Travelers taking 6-8 trips annually who value lounge access

- Points Maximizers: Savvy consumers who track and optimize rewards redemption

- Premium-Curious Shoppers: Those testing premium benefits before committing to expensive cards

Key Features & Benefits

1. Accelerated Rewards on Key Categories

Earn points faster where you spend most:

- 2X Points on dining, groceries, and petrol (2 points per AED 5 spent)

- 1X Points on all other purchases (1 point per AED 5 spent)

- No monthly earning caps—unlimited rewards potential

- Points never expire as long as card remains active

Effective Rewards Rate:

- Dining/Groceries/Petrol: 0.8% (when redeeming for cashback) or 1-1.5% (when redeeming for miles)

- All Other Purchases: 0.4% or 0.5-0.75% (miles redemption)

2. Flexible Redemption Options

Convert FAB Rewards points multiple ways:

- Emirates Skywards Miles: 4 FAB points = 1 Skywards mile

- Etihad Guest Miles: 4 FAB points = 1 Guest mile

- Cashback: 2,000 FAB points = AED 40 cashback

- Vouchers: Redeem for retailer gift cards (Amazon, Mall of Emirates, etc.)

- Merchandise: Catalog redemption for electronics, appliances, luxury goods

Redemption Strategy Tip: Miles conversions typically offer 25-50% better value than cashback. Redeem for Emirates or Etihad miles when booking premium cabins for maximum value.

3. Complimentary Airport Lounge Access

Enjoy Priority Pass membership with generous access:

- 6 free lounge visits per year (vs 4 for most comparable cards)

- Access to 1,300+ lounges worldwide

- Includes Dubai International, Abu Dhabi, Sharjah, and all major UAE airports

- Additional visits at USD 32 (~AED 117) per entry

- Guest access available at additional cost

Annual Value: 6 lounge visits × AED 130 average value = AED 780—more than your annual fee from year two.

4. Travel Insurance Coverage

Comprehensive travel protection when booking with the card:

- Up to AED 350,000 overseas medical emergency coverage

- Up to AED 15,000 baggage loss/delay protection

- Up to AED 7,500 trip cancellation/interruption coverage

- Up to AED 350,000 personal accident cover

- Coverage for cardholder, spouse, and dependent children

- 180-day maximum trip duration

5. Purchase Protection & Extended Warranty

- 90-day purchase protection against theft or accidental damage (up to AED 3,000 per claim)

- Extended warranty: Adds one year to manufacturer warranties on eligible items

6. Complimentary Golf Rounds

Enjoy 1 complimentary golf round per year at participating UAE golf courses (subject to availability).

7. Contactless Payments & Digital Wallets

Full support for Apple Pay, Samsung Pay, Google Pay, and NFC transactions.

8. Zero Liability Fraud Protection

Not responsible for unauthorized transactions reported promptly.

Fees & Charges Breakdown

| Fee Type | Amount |

|---|---|

| Annual Fee (Year 1) | FREE |

| Annual Fee (Year 2+) | AED 500 |

| Interest Rate | 2.99% per month (~36% APR) |

| Late Payment Fee | AED 230 |

| Cash Advance Fee | 4% (min AED 100) |

| Foreign Transaction Fee | 2.5% |

| Supplementary Card Fee | AED 250/year each |

| Extra Lounge Visit | USD 32 (~AED 117) per visit |

Fee Waiver Opportunity: Many cardholders successfully negotiate annual fee waivers by calling retention before renewal and mentioning competitor offers or high monthly spend.

ROI Analysis: Will You Come Out Ahead?

Scenario 1: Moderate User (AED 8,000/month total spend)

- Dining/Groceries/Petrol: AED 3,500 × 0.8% = AED 28/month

- Other: AED 4,500 × 0.4% = AED 18/month

- Annual Rewards Value (cashback): AED 552

- Lounge Access: 6 visits × AED 120 = AED 720

- Total Annual Value: AED 1,272

- Net Profit (Year 2+): AED 772 (after AED 500 fee)

✅ Good Value – Solid return even with moderate spending.

Scenario 2: Active User (AED 15,000/month total spend)

- Dining/Groceries/Petrol: AED 6,000 × 0.8% = AED 48/month

- Other: AED 9,000 × 0.4% = AED 36/month

- Annual Rewards Value (cashback): AED 1,008

- Lounge Access: 6 visits × AED 130 = AED 780

- Total Annual Value: AED 1,788

- Net Profit (Year 2+): AED 1,288

✅ Excellent Value – Nearly 3.5x return on annual fee.

Scenario 3: Miles Redeemer (AED 15,000/month, converting to Emirates miles)

- Annual Points Earned: ~360,000 points

- Convert to Emirates: 90,000 Skywards miles

- Miles Value (assuming 4 fils/mile economy, 10+ fils/mile premium): AED 3,600-9,000

- Lounge Access: AED 780

- Total Annual Value: AED 4,380-9,780

- Net Profit (Year 2+): AED 3,880-9,280

✅ Outstanding Value – Miles redemption multiplies value dramatically.

Breakeven Point: Spend just AED 5,200 monthly (AED 62,500 annually) to earn AED 500 in rewards—covering your year-two annual fee. Add lounge access, and breakeven drops to roughly AED 3,500/month.

How It Compares to Competitors

vs. Standard Chartered Platinum Credit Card

- Winner: Standard Chartered for cashback rate (5% vs FAB’s 0.8% on dining/groceries)

- Winner: FAB Rewards Signature for lounge access (6 visits vs none)

- Winner: FAB Rewards Signature for miles flexibility (can convert to Emirates or Etihad)

- Verdict: If you want pure cashback, Standard Chartered wins. For travel perks + flexible redemption, FAB Rewards Signature is better.

vs. Emirates NBD Skywards Signature Credit Card

- Winner: Emirates NBD for Emirates-exclusive flyers (higher miles earn rate on Emirates)

- Winner: FAB Rewards Signature for multi-airline travelers (can redeem for Emirates OR Etihad)

- Winner: FAB Rewards Signature for lower annual fee (AED 500 vs AED 750)

- Verdict: Emirates loyalists should stick with Emirates NBD. For flexibility, FAB Rewards Signature offers better value.

vs. Mashreq Platinum Elite Credit Card

- Winner: Mashreq for Smiles points integration (if you’re a Smiles member)

- Winner: FAB Rewards Signature for international lounge access (Priority Pass vs Mashreq’s limited partnerships)

- Winner: FAB Rewards Signature for travel insurance (AED 350k vs AED 250k)

- Verdict: Both are solid mid-tier cards. Choose based on whether you prefer Smiles points (Mashreq) or Emirates/Etihad miles (FAB).

10 Expert Tips to Maximize This Card

- Convert Points to Miles for Premium Cabins: Your 90,000 Emirates Skywards miles can book business class flights worth AED 15,000+. This is 3-5x better value than cashback redemption.

- Use for All Grocery Shopping: The 2X points on groceries means every Carrefour, Lulu, and Spinneys trip earns double. Route ALL household grocery spending through this card.

- Book Restaurants via Zomato/Deliveroo with Card: Earn 2X points on food delivery and takeout, not just dine-in. Stack with platform discounts for maximum savings.

- Fuel Up Consistently at the Same Station: Earn 2X points on petrol. If you drive 2,000km/month (~400L fuel at AED 2.80/L = AED 1,120), that’s AED 450 points monthly just from fuel.

- Never Carry a Balance: At 36% APR, interest obliterates rewards value. Always pay in full by due date.

- Book Lounge Access in Advance: Use the Priority Pass app to reserve lounge spots 24-48 hours before flights, especially during peak seasons.

- Wait for Transfer Bonuses: Occasionally, FAB offers bonus point conversions (e.g., 3 points = 1 mile instead of 4). Transfer your points during these promotions for 33% more miles.

- Don’t Use Abroad: The 2.5% FX fee eats into rewards. Get a no-FX-fee travel card for international spending.

- Track Your Points Balance Monthly: Log into FAB Rewards portal regularly. Points don’t expire, but you should transfer in batches of 10,000+ to avoid small transfer inefficiencies.

- Pair with a No-Fee Cashback Card: Use FAB Rewards Signature for categories earning 2X points. Use a fee-free cashback card (Liv, HSBC Live+) for everything else to maximize overall returns.

Potential Drawbacks & Considerations

1. Lower Cashback Rate Than Specialist Cards

At 0.8% effective cashback on bonus categories, this card trails specialist cashback cards offering 5-10% in specific categories. However, the lounge access and miles flexibility compensate.

2. Supplementary Card Costs

At AED 250/year per supplementary card, adding family members is expensive compared to competitors offering free supplementary cards.

3. Foreign Transaction Fee

The 2.5% fee makes this card uneconomical for international spending. Stick to AED-denominated purchases only.

4. Miles Conversion Rate

4 FAB points = 1 airline mile is decent but not spectacular. Some cards offer 3:1 or even 2:1 during promotions.

5. Income Requirement

Minimum salary of AED 15,000/month excludes mid-level professionals and entry-level managers.

6. Limited Luxury Perks

No concierge service, hotel status upgrades, or luxury experiences like higher-tier cards (Amex Platinum, Emirates Infinite).

How to Apply: Step-by-Step Guide

Eligibility Requirements

- Minimum age: 21 years

- Minimum salary: AED 15,000 per month (salaried) or AED 180,000 annual income (self-employed)

- UAE residency: Valid UAE residence visa

- Employment: Minimum 6 months with current employer (3 months for government employees)

- Credit score: Good standing

Required Documents

- Copy of valid passport with UAE residence visa

- Copy of Emirates ID (both sides)

- Latest 3 months’ salary certificates or bank statements

- Proof of address (utility bill, tenancy contract, or bank statement)

- For self-employed: Trade license and 6 months’ bank statements

Application Process

- Online Application: Visit bankfab.com and locate the Rewards Signature Card page. Complete online form (15-20 minutes)

- Document Submission: Upload documents via online portal

- Bank Review: FAB reviews your application (2-5 business days)

- Approval & Card Production: Card produced and couriered (5-7 business days)

- Activation: Activate via FAB Mobile app, online banking, or phone

- Priority Pass Enrollment: Your Priority Pass card arrives separately within 2-3 weeks. Activate at prioritypass.com

Pro Tip: Existing FAB Priority Banking customers often get instant approval and can negotiate better terms. If you maintain AED 50,000+ in your FAB account, mention it during application.

Frequently Asked Questions

Q: Do FAB Rewards points expire?

A: No, points never expire as long as your card remains active. However, if you cancel the card, you typically forfeit unused points, so redeem before canceling.

Q: Can I transfer points to both Emirates and Etihad in the same year?

A: Yes, you can split your points between programs. For example, transfer 50,000 points to Emirates (12,500 miles) and 50,000 to Etihad (12,500 miles) if desired.

Q: How long does miles conversion take?

A: Typically 5-7 business days from request to miles appearing in your airline loyalty account. Plan ahead if booking flights.

Q: Is there a minimum redemption amount?

A: Yes, most redemptions require at least 2,000 FAB Rewards points (equivalent to AED 40 cashback or 500 airline miles). Check the rewards portal for specific thresholds.

Q: Can I use Priority Pass for guests?

A: Yes, but guests are charged separately (typically USD 32/guest). Only the primary cardholder gets 6 free visits.

Q: Does the 2X points apply to online grocery delivery?

A: Yes, as long as the merchant is coded as a grocery/supermarket (like Carrefour.ae, Instashop orders from Spinneys, etc.). Food delivery apps like Zomato/Deliveroo also earn 2X as dining.

Q: What happens to my points if I upgrade to a different FAB card?

A: Points typically transfer to your new FAB card automatically. Confirm with FAB before upgrading to avoid any issues.

Q: Can I gift my points to someone else?

A: No, FAB Rewards points are non-transferable between cardholders. However, once converted to airline miles, you can use those miles to book flights for anyone.

Final Verdict: Should You Get This Card?

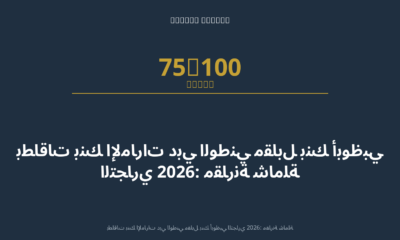

The FAB Rewards Signature Credit Card earns a strong 83/100 rating—making it one of the best mid-tier rewards cards in the UAE for value-conscious travelers and flexible spenders.

✅ Get This Card If:

- You spend AED 10,000+ monthly and want flexible rewards redemption

- You fly both Emirates and Etihad (or switch between airlines)

- You want airport lounge access without paying AED 1,500-3,000 annually

- You earn AED 15,000+ monthly and meet the income requirement

- You want premium-tier benefits at a mid-tier price point

- You value redemption flexibility over maximum rewards rate

❌ Skip This Card If:

- You always pay in full and want maximum cashback (get a specialist cashback card instead)

- You’re exclusively loyal to Emirates (Emirates NBD Skywards card offers better Emirates-specific value)

- You can’t meet the AED 15,000 monthly income requirement

- You rarely travel and won’t use lounge access

- You spend heavily abroad (2.5% FX fee makes this expensive internationally)

The Bottom Line

The FAB Rewards Signature Credit Card succeeds where many cards fail: it offers genuine premium value without the premium price tag. Its combination of accelerated rewards on everyday spending, generous lounge access, and exceptional redemption flexibility creates a compelling package for UAE professionals.

Where this card truly shines is its “have your cake and eat it too” approach. Want cashback? Convert to cash. Planning a honeymoon? Transfer to Emirates miles for business class. Fly Etihad more? Redirect points there instead. This flexibility is rare—most cards lock you into one program or redemption type.

If you’re spending AED 10,000-20,000 monthly anyway, routing that through the FAB Rewards Signature nets you 1,500-3,000 in annual value (rewards + lounge access)—making the AED 500 fee trivial. And if you’re strategic about miles redemptions, you can extract 3-5x that value booking premium cabin flights.

Overall Rating: 83/100 – Highly Recommended for flexible travelers and rewards optimizers

فريق المراجعة التحريرية

أحمد حسن، CFP® – الكاتب الرئيسي

مخطط مالي معتمد مع 12+ سنة خبرة في الاستشارات المصرفية والتخطيط المالي في الإمارات. حاصل على شهادة CFP® من معهد التخطيط المالي المعتمد.

سارة الخالدي – مدققة الحقائق

محللة مالية معتمدة (CFA Level II) مع 8 سنوات خبرة في التحقق من البيانات المالية ومقارنة المنتجات المصرفية في دول الخليج.

محمد عبدالله – المراجع

خبير في بطاقات الائتمان وبرامج الولاء في الشرق الأوسط، 15+ سنة في القطاع المصرفي، ومستشار سابق في Emirates NBD وADCB.

إنجي – رئيسة التحرير

رئيسة تحرير Voyage Arabia، مسؤولة عن ضمان جودة المحتوى والتزامه بمعايير E-E-A-T وسياسات YMYL للمحتوى المالي.

-

الإمارات العربية المتحدةشهرين ago

الإمارات العربية المتحدةشهرين agoبطاقة Etihad Guest Visa Infinite Covered Card من بنك أبوظبي الإسلامي – مراجعة شاملة 2026

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقات بنك الإمارات دبي الوطني مقابل بنك أبوظبي التجاري 2026: مقارنة شاملة

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة DIB Emirates Skywards Platinum Covered الائتمانية

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة DIB SHAMS Platinum Covered الائتمانية

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة FAB Etihad Guest Infinite Islamic الائتمانية

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة FAB Blue FAB Islamic الائتمانية

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة FAB SHARE Platinum الائتمانية

-

بطاقات الائتمانشهرين ago

بطاقات الائتمانشهرين agoبطاقة HSBC Gold الائتمانية